Taking a loan is a significant financial decision that requires careful consideration. Whether it’s for purchasing a house, financing higher education, or consolidating debt, loans can be helpful in achieving financial goals. However, it’s essential to understand the key factors before committing to a loan. Here are some important things to keep in mind when taking a loan.

Loan Type and Purpose

The first step is to determine the type of loan you need and its purpose. Different loans serve different needs. For instance, home loans, personal loans, car loans, and education loans have varying terms and interest rates. Knowing what you need the loan for helps you choose the best loan type and avoid unnecessary borrowing.

Interest Rates and Terms

Interest rates play a critical role in how much you’ll pay over the life of the loan. Loans can have either fixed or floating interest rates. Fixed rates remain constant throughout the loan tenure, while floating rates can change based on market conditions. It’s essential to understand how interest rates work and choose one that fits your financial situation. Make sure to compare rates from different lenders to ensure you’re getting the best deal.

Loan Tenure

The loan tenure is the period over which you’ll repay the loan. Longer tenures typically result in lower monthly payments but may lead to higher overall interest payments. On the other hand, shorter tenures may require higher monthly payments but save you money in the long term. Choose a tenure that you can comfortably manage within your budget.

Repayment Ability

Befor taking a loan, assess your repayment capacity. Consider your income, monthly expenses, and other financial obligations. A loan should not burden you financially. Ensure that you can comfortably repay the loan without affecting your daily expenses or quality of life. Having a clear understanding of your financial situation can help you avoid defaulting on the loan.

Processing Fees and Hidden Charges

Many lenders charge processing fees, administrative fees, and other hidden charges. Make sure to ask about any additional fees before finalizing your loan agreement. It’s important to consider these costs as they can add up and increase the overall cost of borrowing.

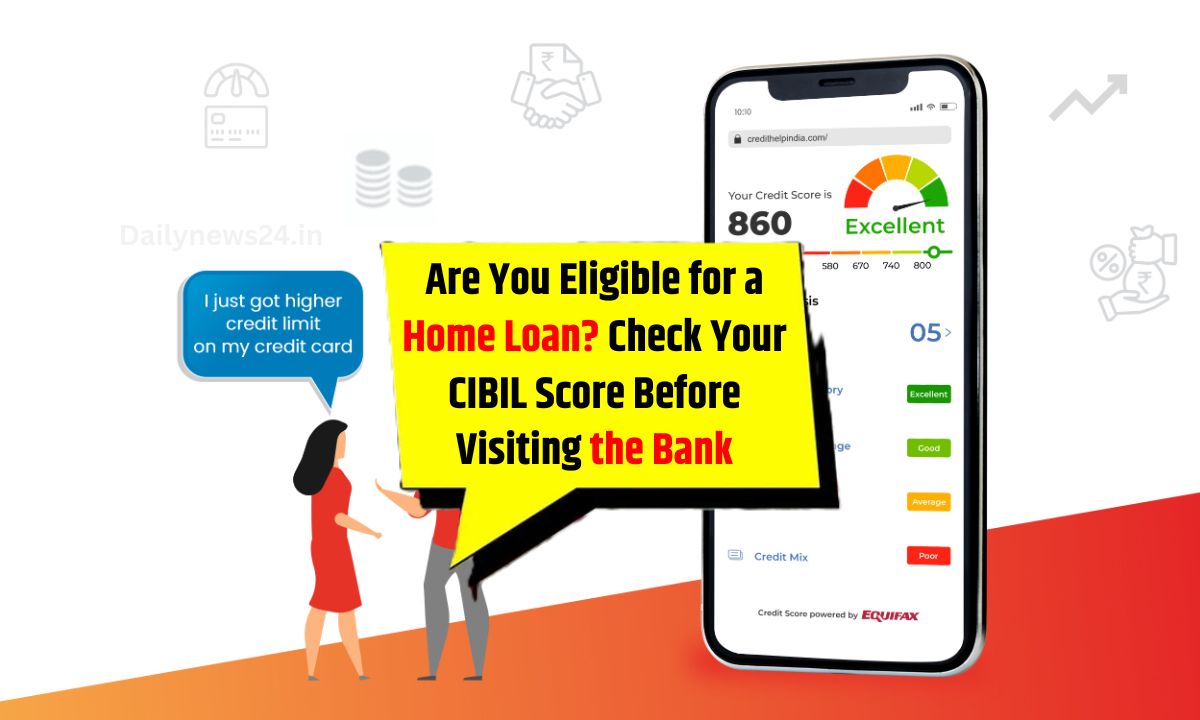

Credit Score

Lenders usually check your credit score before approving a loan. A higher credit score increases your chances of getting approved and may help you secure a lower interest rate. If your credit score is low, it may be a good idea to improve it before applying for a loan. Paying off existing debt and maintaining a good credit history can go a long way.

Prepayment and Foreclosure Options

Check whether your loan allows for prepayment or early settlement without penalties. Some loans come with prepayment charges, so it’s important to be aware of the terms regarding this. If you receive a financial windfall or want to pay off the loan early, having the option to do so can save you interest.

Also Read

Top Online Earning Apps in 2025 Make Money from Your Smartphone

Win ₹500 Daily Play and Earn Real Money Online No Investment Needed

7 Powerful Ways to Earn Money from Instagram in 2025

Dailynews24 App :

Read the latest News of Country, Education, Entertainment, Business Updates, Religion, Cricket, Horoscope Here. Read Daily Breaking News in English and Short Video News Covers.